Quick Answer

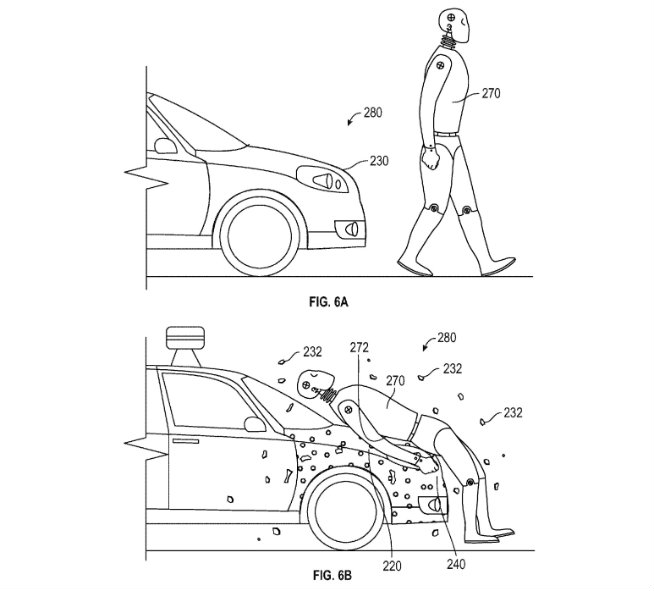

For a pedestrian unlucky enough to be hit by one of Google's self-driving cars, the company has received a patent for a potentially life-saving solution: the impact of a crash would expose a sticky layer of adhesive on the hood which the victim would adhere to, potentially avoiding further injury from secondary impacts (e.g. getting thrown from the vehicle and hitting the roof of the car, road or other hard surface).

Although this unusual (and morbidly amusing) human flypaper concept may never come to life, it's a reminder of the astounding progress that has been made with self-driving or autonomous vehicles (defined as having features that allow them to accelerate, brake, and steer a vehicle's course with limited or no driver interaction).

This article covers changes to the personal injury economy that could occur with the growth of the autonomous vehicle industry.

Autonomous vehicles (AVs) are an uncertain frontier for regulators and insurers, who have established century-old rules based on human driving behavior. The technologies under the hood use sophisticated sensors, computer software, and cameras to guide vehicles, dictate speed, and brake without driver intervention.

AVs hold the promise of safer driving, but they also raise important questions for legal funders, such as the allocation of liability in the event of an AV crash. The inevitable proliferation of AVs will present unprecedented market opportunities and a dramatic reduction of costs related to motor vehicle accidents (MVAs). This creates uncertainty for any profession tied to the personal injury industry, including legal funders, doctors, lawyers, and insurance companies.

STATE OF THE INDUSTRY

AVs have captivated the auto industry in recent years, sparking a race between a wide variety of companies to develop them. Just last year, Delphi’s autonomous car drove itself across the country, reportedly handling 99% of the 3,400 mile journey from San Fransisco to New York on its own. Google has test driven its fleet of self-driving vehicles in autonomous mode for 1.5 million miles since 2009.

Most of the world’s major automakers are working on autonomous technology, many of which aim to put self-driving autos on the roads by 2020. The ride-hailing giant Uber began testing self-driving cars in May 2016, and Uber’s CEO has indicated that consumers can expect a driverless Uber fleet by 2030.

And it’s not just cars— one startup is focused on putting self-driving big rigs on the road, building a hardware kit that would allow retrofitted trucks to handle highway driving while a human driver naps or handles other tasks. Other companies are working on similar technology for buses.

Explosive growth in the still-nascent industry seems inevitable. One estimate puts 10 million self-driving cars on the road by 2020. Other experts anticipate that up to 75% of all vehicles will be autonomous by 2040, and the US Secretary of Transportation expects driverless cars to be in use worldwide within the next 10 years.

RAMIFICATIONS FOR THE "PERSONAL INJURY ECONOMY"

1. FEWER ACCIDENTS

As Chunka Mui noted in a 2013 Forbes series about driverless cars, human error is responsible for roughly 90% of MVAs. In 2014, moreover, the U.S. was home to more than 5 million MVAs, killing 32,675 people and injuring more than 2.34 million. Studies have indicated that AVs could reduce accidents by up to 90%.

Google has made a similar claim and, true to form, its self-driving cars have been in just 18 accidents since 2009 (compared to about 5 million non-AV accdents in 2014 alone). In fact, until February 2016, when an autonomous Google car caused a minor crash with a public transit bus, every Google accident was actually caused by human error and not the technology (the cars tend to get rear-ended by human drivers at red lights!).

Nonetheless, a recent incident proves that AVs are certainly not accident proof (yet): U.S. auto-safety regulators are currently investigating the first fatal crash involving a Tesla Motors car that was driving itself. The driver died when his electric car, running on autopilot, drove under the trailer of an 18-wheel truck on a highway. This investigation is likely to spur additional reservations about the progress of automated cars, but there is no question that they are going to be significantly safer than human driving.

Of course, a car doesn't need to drive itself to avoid accidents. Many automakers already incorporate intelligent accident-avoidance and crash-monitoring technology in their vehicles. Volvo, in particular, has made a bold promise that by 2020 there will be no serious injuries or fatalities in a Volvo car or SUV. As this incremental technology gains consumer confidence, it will surely also gain wider use.

2. FEWER HOSPITALIZATIONS AND COSTS

Fewer accidents, of course, means fewer hospitalizations. According to a CDC report, in 2012 more than 2.5 million people went to the emergency department- with nearly 200,000 hospitalized- because of MVA injuries (nearly 7,000 people per day).

Mui estimates that "emergency rooms will lose millions of patients a year, and hospitals would have hundreds of thousands fewer people who needed to stay overnight." Studies indicate that MVAs cost at least $450 billion annually between medical costs, property damage, loss of productivity, legal costs, travel delays, and lost quality of life; Google predicts it could potentially reduce these expenses by $400 billion.

3. MORE TRANSPARENCY

Crash-monitoring technology of the sort used by Google and Volvo means greater accountability in MVAs, and the various cameras and sensors both actively protect drivers and may simplify the process of pinpointing blame for certain crashes, such as those between an AV and regular automobile. This could mean the end of insurance fraud, and possibly the end of low-ball insurance settlements. Mui notes, there will be fewer "gray areas" that require the involvement of personal-injury lawyers. This will naturally lead to...

4. FEWER PERSONAL INJURY CLAIMS

Mui predicts that the proliferation of AVs means "personal-injury attorneys would see car-related cases all but disappear." This might not be so frightening for attorneys, who handle many different types of cases, but it could be devastating for insurers (since insurance rates are calculated based on risk). Here's Mui again:

Auto insurers, which collect more than $200 billion in personal auto premiums each year in the US, would initially see profits rise as accidents declined and payments to customers dropped. They would, however, eventually see something like 90% of premiums disappear. In fact, the US model of mandatory personal auto insurance might become archaic.

Again, the hit will come long before driverless cars dominate the roads. Mui cites insurance veteran Guy Fraker's argument that since the majority of MVAs occur in congested traffic: "even a 25% adoption of incremental driverless technology, such as smart cruise control and crash avoidance" would reduce congestion, and in turn, accidents. Fred Cripe, another insurance industry veteran, clarified the situation in starker terms: Eventually, he predicts, "car insurance goes away."

5. ASSUMPTION OF LIABILITY

Consumer concerns about liability, one of the many unanswered questions that regulators will have to grapple with, could represent a roadblock to acceptance of driverless cars.

Who is to blame in the event that a self-driving car is involved in a crash or hacked by a criminal third party? Modern product-liability law does not contemplate cars without drivers, and owners won't want to be blamed for crashes they couldn't prevent. In response to these concerns, Google and some car manufacturers, including Mercedes and Volvo, have said they will accept full liability whenever one of its cars is in autonomous mode.

Some attorneys, who read these statements as marketing ploys, see opportunity. Before a future of accident-free roads is realized, it's inevitable that the early generations of driverless cars are going to collide with other driverless vehicles and those with accident-prone humans behind the wheel.

With no one behind the wheel, some lawyers theorize that they can go after almost anyone even remotely involved for potentially big payouts: "You're going to get a whole host of new defendants... computer programmers, computer companies, designers of algorithms, Google, mapping companies, even states. It's going to be very fertile ground for lawyers."

6. THE END OF PERSONAL INSURANCE?

As Mui notes, “for decades, insurers have invested heavily in their abilities to assess individual risk and price accordingly.” Intelligent driving technology will diminish the importance of underwriting by removing the majority of human error from MVAs. Insurance companies will have to change their business models to remain competitive or risk being cut out.

AllState’s 2015 annual report warns that AVs could disrupt their business model— the first time that such a risk has been mentioned in the risk section of its annual report— and that it will be very difficult to compensate for the resulting losses to its business model.

And it’s not just auto insurance that stands to suffer; health insurers will see billions in lost revenue as well. The decrease in hospitalizations, meanwhile, means that personal injury attorneys who do take accident-related cases will probably see the value of those cases decrease as well.

FINAL THOUGHTS

AVs will undoubtedly bring about a beneficial sea change in the way we travel, improving motor vehicle safety, reducing traffic congestion and saving fuel and other costs.

At the same time, these exciting developments will bring about a notable shift for anyone involved in the personal injury economy, including financiers of the industry, and it will be important for these professions to keep abreast of further developments in the space.

Photo credit: Rita E via Pixabay

Know Your Claim’s Worth—and Settle It

Serious injury or no injury at all, move your case forward instantly from your phone.

Thank you for submitting your information.

About the author

Joshua is a lawyer and tech entrepreneur who speaks and writes frequently on the civil justice system. Previously, Joshua founded Betterfly, a VC-backed marketplace that reimagined how consumers find local services by connecting them to individuals rather than companies. Betterfly was acquired by Takelessons in 2014. Joshua holds a JD from Emory University, and a BA in Economics and MA in Accounting from the University of Michigan.